Positive outlook for business as credit demand climbs

Veda Quarterly Business Credit Demand Index: December 2016 quarter

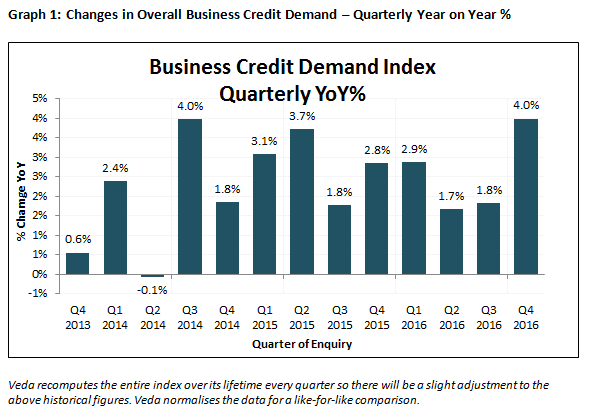

- Overall business credit applications rose +4.0% (vs December quarter 2015)

- Growth in business loan applications rose +5.7% (vs December quarter 2015)

- Rate of growth in trade credit applications and asset finance also rose (vs December quarter 2015)

Sydney, Australia – Tuesday, 24 January 2017: The Veda Quarterly Business Credit Demand Index – measuring applications for business loans, trade credit and asset finance – saw applications rise at an annual rate of +4.0% in the December 2016 quarter.

This rate of growth in business credit demand was buoyed by a recovery in asset finance (+3.0%) and particularly by an increase in business loan applications (+5.7%), supported by the strength of commercial mortgage applications.

Neil Shilbury, Veda General Manager, Commercial and Property Products, said business credit demand in the December 2016 quarter had benefited from the recent low interest rates and the lower Australian dollar.

“Investment in property construction continues to be strong across a number of jurisdictions in Australia as demand for property investment continues by local and foreign investors, despite recent increases in commercial lending rates,” Mr Shilbury said.

“Since the end of the mining boom, there has been a significant lull in business investment. The rise in construction activity has gone some way to fill this gap, though many businesses remain understandably cautious,” Mr Shilbury added.

Although the rate of business credit application growth in non-mining jurisdictions (+5.3%) remained higher than in the mining jurisdictions (+1.1%), conditions in Queensland appear to be improving, helped along by growth in tourism and construction.

“An influx of high-spending tourists attracted by the lower Australian dollar, particularly those from China, has had a visible impact on the business conditions in Queensland. This is reflected in the state’s positive growth in comparison to the other mining jurisdictions,” Mr Shilbury said.

“Queensland has also benefited from the housing construction boom more than Western Australia or the Northern Territory. The spike in property construction, particularly the inner-city suburbs of Brisbane, has helped lift Queensland out of the post-mining slump,” he added.

Released today by Veda, Australia and New Zealand’s leading provider of consumer and commercial data and insights and a wholly-owned subsidiary of Equifax, the Veda Business Credit Demand Index once again showed a disparity between the business conditions of mining and non-mining states.

The Veda Business Credit Demand Index has historically proven to be a lead indicator of how the overall economy is performing. The behaviour seen in the annual rate of growth in business credit applications, illustrated by Veda’s data, suggests an improved economic outlook.

Business loan applications were the strongest performer in the December quarter, continuing the growth seen in the previous quarter. Once again, the increase was driven by mortgage application growth (+22.5%), which has now returned to the strong annual growth rate recorded in the June quarter of 2015.

Growth in overall business credit applications improved in the December quarter (+4.0%). Victoria led the way, with a growth rate of +6.8%. This was followed by the ACT (+6.1%), NSW (+4.4%), Tasmania (+3.6%), and SA (+3.3%). The mining jurisdictions continued to be more subdued, with only Queensland experiencing positive growth (+2.3%). WA (-1.3%) and the NT (-1.0%) both showed falls in the December quarter.

Growth in business loan applications picked up in the December quarter (+5.7%). NSW (+9.2%), Victoria (+8.7%), SA (+3.2%), and the ACT (+1.9%) all reported solid growth in business loan applications, although Tasmania (-2.0%) experienced a fall. Of the mining jurisdictions, WA (+2.6%) was the strongest performer in the December quarter, while Queensland (-0.8%), and the NT (-8.3%) declined.

Within business loans, growth in lending proposals (+7.7%) and mortgage applications (+22.5%) were up in the December quarter, but credit cards (-17.1%), overdrafts (-4.8%), and premium finance (-24.1%) fell.

Trade credit applications recovered in the December quarter (+2.6%). The growth in trade credit applications was strongest in the ACT (+14.1%), followed by the NT (+7.0%), Victoria (+5.4%), SA (+5.0%), Tasmania (+4.0%), Queensland (+4.0%), and NSW (+0.9%). WA (-4.3%) was the only jurisdiction to experience a fall.

The improvement in trade credit applications reflects a lift in the main category of 30 day accounts (+2.3%), which has improved from an annual rate of decline of -0.7% in the September quarter of 2016.

Growth in asset finance applications moved higher in the December quarter (+3.0%). Across the non-mining jurisdictions, growth in asset finance applications remained positive in Tasmania (+11.9%), Victoria (+5.6%), the ACT (+3.4%), NSW (+1.3%), and SA (+1.4%). In the mining jurisdictions, growth in asset finance applications was strongest in Queensland (+5.0%), but fell in WA (-2.5%) and the NT (-3.1%).

There was some differing movement within asset finance account types. Applications for commercial rental (+13.9%) continued to show strength, as did auto loans (+11.2%), leasing (+9.8%) and bill of sale (+28.2%). In contrast, applications for hire purchase (-16.4%) fell sharply for another quarter.

NOTE TO EDITORS

The Veda Quarterly Business Credit Demand Index measures the volume of credit applications that go through the Veda Commercial Bureau by credit providers such as financial institutions and major corporations in Australia. Based on this it is a good measure of intentions to acquire credit by businesses. This differs to other market measures published by the RBA/ABS, which measure new and cumulative dollar amounts that are actually approved by financial institutions.

DISCLAIMER

Purpose of Veda media releases:

Veda Indices releases are intended as a contemporary contribution to data and commentary in relation to credit activity in the Australian economy. The information in this release is general in nature, is not intended to provide guidance or commentary as to Veda’s financial position and does not constitute legal, accounting or other financial advice. To the extent permitted by law, Veda provides no representations, undertakings or warranties concerning the accuracy, completeness or up-to-date nature of the information provided, and specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.