Outlook 2022-23: Change and Opportunities for Mortgage Brokers

Mortgage demand has dropped in the wake of rate hikes and cost of living pressures, but refinancing has hit record highs. James Forbes, General Manager of the Consumer Division at Equifax describes how "Back-to-back mortgage payment rises and increased pressures on household budgets drove 27,667 Australian homeowners to swap lenders in the month of August, a 16% increase on the previous year’s period1." James Forbes explains "how this search for a better home loan will likely continue for an extended period as borrowers come off fixed-rate terms locked in during the record low-interest rate period." James Forbes suggests that "given that mortgage brokers are writing an increasing share of home loans, this wave of residential refinancing will keep mortgage brokers busy for months to come and see intense competition emerge to prevent churn."

Understanding the key themes shaping the mortgage market will help brokers put themselves in the best possible position as trusted experts. Armed with informed insights, brokers can meet Best Interest Duty obligations, and support customers find loans that suit individual needs in an ever-changing landscape. Crucially, a clear view of the present and the future supports greater financial inclusion by helping Australians make smart choices during these difficult and turbulent times.

Here we share where the market stands today, what we know about consumer credit behaviour and financial hardship, and the opportunities and challenges ahead for mortgage brokers.

Economic conditions: where we stand today

A broad range of macro-economic conditions, including cash rate rises, employment, household indebtedness and household savings, influence consumer credit demand in the Australian property market.

Interest rates

During six months of rate rises, interest rates have increased from a low of 0.10% in April to 2.85% in November, with experts predicting more rate rises to come2.

As the cash rate rises, so do household costs – at the fastest pace in 21 years. Food and beverage prices are up by 9%, transport costs by 9.2% and building costs by more than 10%. These increases look set to continue into 2023.

Employment

A positive note amidst the downturn is that unemployment is at historically low levels – the lowest in 48 years. An unemployment rate steady at 3.5% is a welcome counterbalance to the upward trajectory of interest rates and living expenses.

Indebtedness

Australian household indebtedness has also increased. The average loan size in September 2022 was $588K, down from a peak of $618K in January this year but 23% higher than in February 2020 pre-pandemic.

New loans

The total value of new residential loan commitments has declined, falling 8.2% to $25 billion in September 2022 - the fourth consecutive month to see a fall. Despite this decline, the value of loan commitments in September remained well above pre-pandemic levels. For example, owner-occupier loans were 23% higher, and investor loans were 60% higher than in February 2020.

Household Savings

Household savings that surged during the pandemic are now falling as consumption increases, and spending outpaces income growth. The household saving ratio declined from 11.1% in Mar 2022 to 8.7% in June 2022, remaining slightly above pre-pandemic levels.

Property

Across the combined capital cities, the volume of property for sale has fallen 43% in late November compared to the previous year’s period. Auction clearance rates are also down by 63.7% -- around ten percentage points below the rate recorded in the same period last year.

Simultaneously, median house prices have dropped across five state capitals, which means that some households face the prospect of negative equity. New home buyers are particularly vulnerable, having taken advantage of 5% deposit incentives but not yet had time to pay down their loans or build equity.

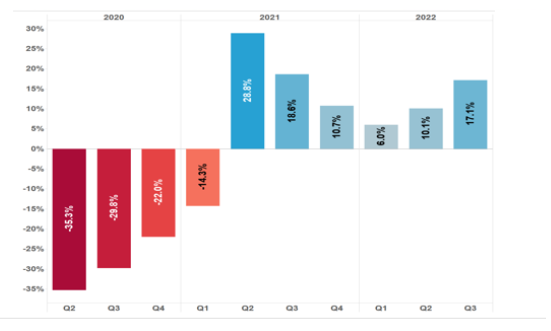

Consumer credit demand: Refinancing wave + rising unsecured debt

Some Australians are turning to unsecured credit as the cost of living increases, the impact of interest rate rises hits home, and household saving buffers dwindle.

Consumer Credit Demand by Qrt vs the Previous Year.

(Source: Equifax)

Quarterly Demand Change (vs same Qtr 2021/22) (Source: Equifax)

(Source: Equifax)

Growth in consumer credit

The Equifax Consumer Credit Demand Index shows consumer credit applications increased by 17.1% in the September quarter compared to the same quarter last year. The index measures the volume of credit applications for credit cards, personal loans, Buy Now Pay Later (BNPL) and auto loans. It is a lead consumer spending indicator because, unlike other market measures, it represents consumers' intention to acquire credit and, in turn, spend.

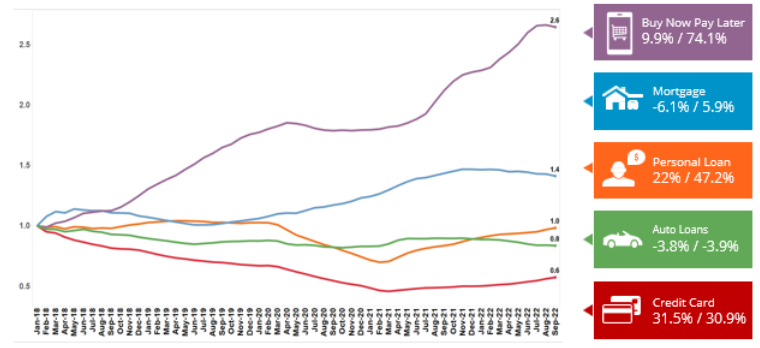

Strong credit card demand

Credit card demand was the primary driver behind overall credit demand in Q3 2022. Compared to the same period last year, demand was up by 31.5%, a trend visible across all states and territories in Australia.

Credit card usage is being fuelled by a return to regular spending habits and an increase in domestic travel post-Covid, but also by Australians turning to unsecured credit to deal with the household budget squeeze.

Increased personal loan demand

As another form of unsecured debt, personal loan applications are also rising. In the September quarter, demand was up by 22% compared to the previous year's period. Growth was particularly evident in NSW and Victoria.

With the Consumer Price Index (CPI) up 1.8% in the September quarter and the cost of renting and furniture skyrocketing3, these rises indicate the type of spending fuelling demand for unsecured credit.

BNPL continues to grow

Young adults, particularly Gen Z, are fuelling BNPL growth. However, demand has slowed, with the volume of BNPL applications down compared to previous quarters, growing by only 9.9% in September. The number of new BNPL entrants has also slowed over the past six months. With the government flagging stricter regulations to bring BNPL in line with credit cards and other credit products, the sector has interesting times ahead.

Decreased auto loan demand

Ongoing supply chain issues have contributed to weak demand for auto loans, with demand dropping by 3.8% in the September quarter compared to the previous year's period. Even a strong performance by the used car market has not offset the decline in new vehicle sales; however, this is likely to change as stock levels become more reliable.

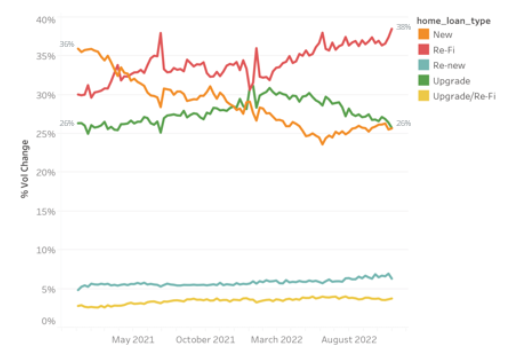

High volumes of refinancing amid reduced mortgage demand

Mortgage Demand by Home Loan Type, Equifax Consumer Credit Demand Index.

(Source: Equifax)

Although mortgage demand has fallen this year (-6.1% in Sept 22), we expect to see high refinancing volumes into 2023 as consumers continue to feel the pinch and look to consolidate their finances. In August 2022, $14 billion worth of home loans were placed with a new lender and refinancing as a percentage of all home loans surged to 38%4.

Borrowers who fixed their mortgages in the past few years will continue to roll off them in the coming years. When their loan reverts to a variable rate considerably higher than their fixed rate, borrowers will have more incentive as they need to seek a better deal. This heightened demand is expected to spurn an increase in competitive offers from lenders keen to retain customers and win refinancing opportunities.

The share of new loans has dropped in line with the growth in house prices. This loan category now sits at around 26% of all home loans. By contrast, new home loans were the dominant form of loan in early 2021, accounting for about 36% of all home loans. With fewer new loan applications, lenders are expected to increasingly focus on actively seeking to retain customers. Improved margins from interest rate increases will provide the scope to offer discounted rates to keep good customers.

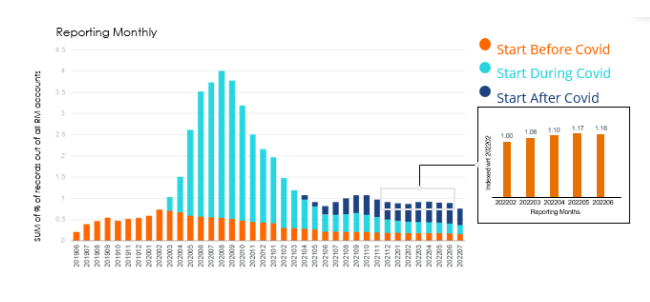

Financial hardship: a rocky road ahead for homeowners

Financial assistance through the pandemic

(Source: Equifax)

Australians who have never previously had financial difficulty are now showing signs of mortgage stress. This new wave of homeowners requiring financial assistance is represented by dark blue on the chart and shares these characteristics:

- opened mortgage accounts during or after Covid

- bought into the housing market at the peak when interest rates were at all-time lows

- typically have good credit scores ranging between 700-1000

- Are less than 45 years of age

- Have higher than average loan limits

- were previously up to date with mortgage repayments and didn’t experience a hardship event during the pandemic.

Even though overall mortgage arrears (30+ Days Past Due (DPD)) rates are still below pre-Covid levels, there has been a gradual increase of 16% in the number of accounts requiring assistance over the past six months. These homeowners have high levels of indebtedness and haven't yet built equity. Their mortgage stress has not yet become mortgage arrears, so time will tell whether they recover or start down the slippery slope to financial hardship.

As of July this year, financial hardship 'flags' are recorded on consumer credit reports.

In practice, when a borrower enters a financial hardship agreement, the repayment history information on their credit report will reflect what was agreed upon under the financial hardship arrangement. For example, suppose the lender agrees to receive half the amount of a consumer's regular repayments. In that case, their credit report will show that the payment has been made if they meet the amount stated in the agreement - rather than displaying missed payments because they're not paying the regular amount.

Making these newly agreed repayments on time each month is a way consumers can demonstrate recovery from hardship.

Mortgage brokers will see hardship flags when checking customers' credit reports, and this extra insight will give brokers a more holistic view of their customers' financial situations. While a hardship flag doesn't automatically preclude a consumer from getting a loan, it can help brokers understand their customer’s vulnerabilities and make informed decisions about how much a customer can repay without overcommitting and which lenders best suit them.

Click here for an infographic summarising the key takeaways outlined in this blog.

Build authority and trust with Equifax digital mortgage broker solutions. Be the broker that helps Australians make smart loan decisions during turbulent times.

To learn more about our mortgage broker tools and solutions Check out our website or Contact our team today.

1Australian Bureau of Statistics

2https://www.afr.com/policy/economy/rate-expectations-drop-after-rba-senate-appearance-20221110-p5bx4f

3Australian Bureau of Statistics, Consumer Price Index, Australia, Sept Qtr 22

4Australian Bureau of Statistics, Lending Indicators, Sept 2022